This blog post highlights how Cambodian community-based organizations are adopting digital tools to strengthen financial inclusion through savings groups. Working with Outreach International and its local partner HURREDO, five groups piloted DreamSave, a mobile application developed by DreamStart Labs, to replace paper records with a digital system. Leaders reported significant benefits: time savings, fewer errors, stronger group accountability, and new digital skills that built their confidence with technology. They also navigated challenges such as limited internet connectivity and older phones, often relying on practitioner support. The experience underscores that while digitization requires patience, it can transform group participation and trust. For practitioners and technology providers, this case offers practical insights into the opportunities and challenges of introducing fintech solutions in rural contexts.

Key Takeaways

- DreamSave has helped Cambodian savings groups save time, reduce errors, and improve transparency.

- Leaders faced challenges with internet connectivity, devices, and following new processes, but learned through persistence.

- Using the app boosted leaders’ digital confidence and encouraged greater participation from group members

Take Action

- Support groups in practicing regularly with digital tools–confidence grows with use.

- Encourage peer-to-peer learning so leaders can share practical tips with each other.

- Invest in patient, community-led adoption: the process takes time, but the payoff is lasting.

Despite Cambodia’s recent economic growth, financial exclusion remains a challenge. According to the National Bank of Cambodia, 41% of adults still lack access to formal financial services, leaving families reliant on informal systems that are often insecure or predatory. Community savings groups offer an alternative, giving members a safe place to save, borrow, and invest in their futures. When HURREDO, a Cambodian NGO and partner of Outreach International, introduced the DreamSave app to community-based organizations (CBOs) in 2023, it marked an important step: a chance to digitize records, improve transparency, and build confidence in financial management.

Laying the Groundwork

Since 2018, Outreach International has partnered with HURREDO to establish eight CBOs in rural Cambodia. Through discussions guided by HURREDO staff, communities identified their shared need for more lucrative livelihood activities. Savings-led microfinance programs offered a way forward, with evidence showing their potential to improve household business outcomes and empower women. Unlike many other microfinance ventures, these savings groups are community led and owned. Leaders undergo financial training so they can plan and manage projects themselves, and all of the capital they access comes in the form of grants rather than loans, keeping resources circulating in the communities.

In 2023, with HURREDO’s support, the groups started their savings journey, joining thousands worldwide. From the outset, we encouraged them to adopt digital tools, following global trends of digital savings groups. The leaders were ready, HURREDO’s practitioners were prepared to guide them, and we at Outreach International were eager to assist. However, we encountered a hurdle: at the time, digital savings group applications were not available in Khmer or using the Riel.

DreamStart Labs and DreamSave

Looking at digital savings applications used globally, we found that DreamStart Labs had already deployed their application, DreamSave, in neighboring Thailand, Vietnam, and the Philippines. Seeing an opportunity for collaboration, we approached DreamStart Labs to explore adapting their application for Cambodia. They agreed, and with the support of their international trainers and engineers, HURREDO translated the app into Khmer. All five CBOs operating at the time agreed to test different versions, providing feedback that shaped the final product.

Following several test runs, HURREDO and their community partners officially launched DreamSave toward the end of 2023. As of September 2025, the five groups have 303 members who have collectively saved more than $11,000 USD. This progress reflects both the value of the DreamStart Labs partnership and the commitment of HURREDO practitioners and grassroots leaders. To better understand the impact of these digital savings and loans groups, in May 2025 we interviewed 10 CBO leaders who regularly use DreamSave.

From Paper to Phones

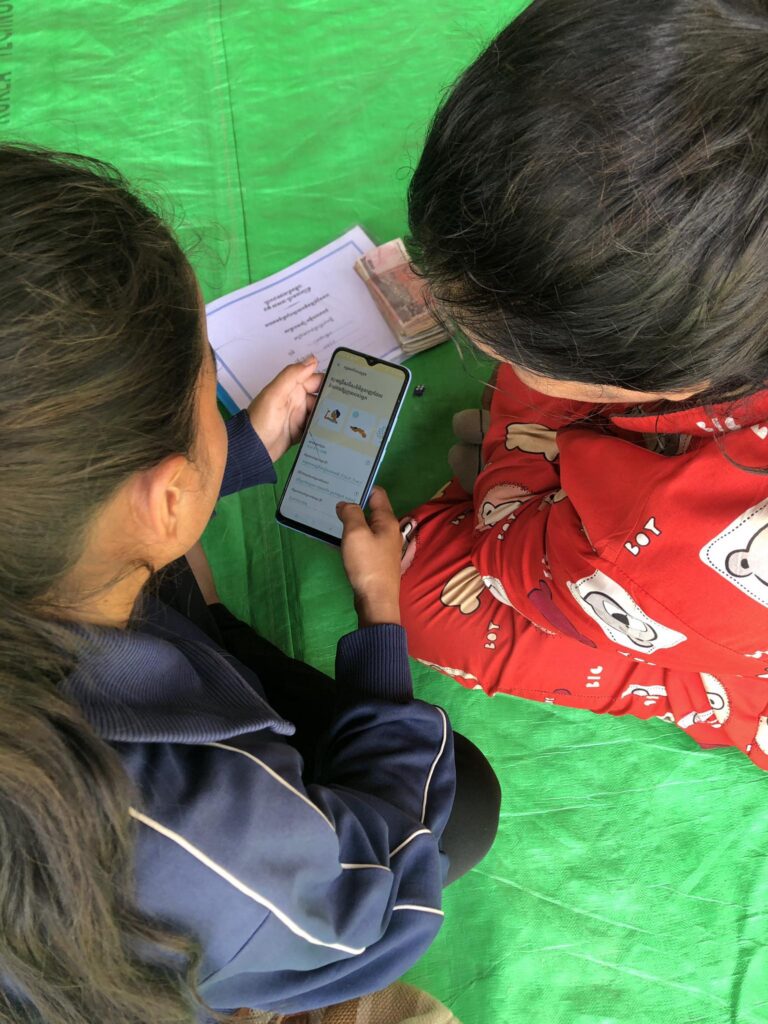

Before going digital, leaders relied on pen-and-paper ledgers to track deposits, loans, and repayments–a slow, error-prone process. DreamSave changed that. Leaders described how automatic calculations saved them time and how they no longer have to enter the same information in multiple places. The application also provided data security: even if a phone is lost or broken, the records remain safe.

“I prefer using DreamSave because it’s easy to click, just click and we can review the amount of savings of each member,” said សែម មករា (Sem Makara), one of the local leaders. “The members themselves are also able to see their amount of savings (on their mobile phones).”

This visibility matters. Members can check their balances through the app, reassuring them that the group’s finances are transparent and accurate. This accountability goes both ways, as leaders can easily identify who has not yet deposited their savings and follow up. Leaders also added that the ability to share records with donors and other stakeholders has strengthened the group’s accountability beyond the community.

The Learning Curve

Of course, no transition is seamless. Leaders faced challenges ranging from poor internet connections to using older phones that struggled to run the app. Some accidentally lost data by clicking out of the app before saving, forcing them to re-encode information. Others were initially confused by certain functions like calculating loan interest or adding new members.

Still, they persisted. Some continue to verify their digital calculations on paper. Others intentionally hold group meetings in places with strong internet connections to ensure the data is fully backed up. Many lean on each other, or program staff, for support and regularly practice using the application to increase their comfort.

As ឆម ជឿង (Chhorm Choerng) described, “When my smartphone has an error, firstly I just calm down and wait until it works, secondly I uninstall other unnecessary apps, and thirdly I ask other users and also HURREDO staff to support.”

Over time, leaders have grown more comfortable with the app, and have also gained broader digital confidence. Every leader interviewed said that they had developed new skills through using DreamSave. Some were tied directly to the app: entering data, reviewing records, or using passcodes. Others were broader: more organized meetings, clearer note-taking, and increased comfort with smartphones.

Strengthening Collective Engagement

As leaders became more confident, they noticed a shift within their groups. Because members could see their balances, they felt more connected to the process. Instead of finances being the responsibility of one record-keeper, the group as a whole became engaged in monitoring progress. Members came to meetings better informed and more invested in collective goals. Yet leaders acknowledged a limitation: not everyone owns a smartphone, meaning some members cannot view their balances. Even with this challenge, the overall effect has been positive. By shifting financial management from a private task into a group effort, DreamSave became more than an accounting tool–it became a catalyst for collective empowerment.

Turning Savings into Opportunity

The impact of these savings groups extends beyond financial recordkeeping. The ultimate goal of the project is to improve members’ economic wellbeing. To this end, groups incorporated a loan program into their structure. Members borrow from the collective savings and repay with interest, which grows the fund for the group as a whole.

These loans have been used in diverse ways: to raise livestock, grow vegetables, and buy rice seeds; to cover transportation costs that make wage-work accessible; and to expand or upgrade small businesses. The combination of collective savings and microloans is helping families both meet immediate needs and plan for the future.

Looking Ahead

Every leader we interviewed said that they plan to continue using both the savings groups and DreamSave for the foreseeable future. They described the app as secure, transparent, and efficient. When asked what advice they would give to others, leaders emphasized the value of regular practice, recommended filling out every section so that the records are complete, and highlighted the need for a reliable internet connection. A common thread through their stories was the willingness to seek help. Whether turning to peers or program staff, this openness to support proved essential to learning.

Looking forward, HURREDO is preparing to launch three more savings-led microfinance programs, and DreamSave will be incorporated from the start. Current groups, meanwhile, are eager to expand. In response to a growing demand for loans and an interest in including more savers, leaders have begun connecting with international funders and foundations to seek out additional resources.

At the same time, HURREDO and its community groups are leveling up their interventions through financial literacy training, which they anticipate will be delivered in collaboration with Good Return. These trainings will follow a Training of Trainers (ToT) model, equipping leaders with the skills to train fellow community members. By strengthening participants’ capacity to strengthen others, the benefits extend beyond the initial training. This peer-to-peer approach creates exponential impact, with each leader multiplying the reach of their knowledge. These ripple effects help scaffold communities for resilience and long-term sustainability.

Conclusion

The experience of these Cambodian leaders shows that digitization is not a straight path, but a process of learning and adapting. DreamSave has helped make savings groups more transparent and efficient, but just as importantly, it has strengthened cooperation and collective accountability. By combining persistence with openness to support, leaders and members are not only managing their savings more effectively, they are also laying the groundwork for stronger communities. Looking ahead, continued collaboration with DreamSave and the addition of financial literacy training through Good Return will sustain this momentum and expand the long-term impact of community-led development.